When Financial Trust Fails, Loyalty Disappears Overnight

The fastest way to lose a customer isn’t through fees or service—it’s through fear. One breach. One stolen identity. One financial product without built-in protection.

In a world where identity theft impacts over 40 million people a year, offering unsecured financial services is no longer a business risk—it’s a brand destroyer. That’s why more banks, credit unions, and fintechs are embedding identity protection directly into their offerings. Not as an upsell. As a must-have.

🔐 Quick Summary: Why Identity Protection Matters

In today’s threat-heavy landscape, the fastest way to lose a customer isn’t a poor app or hidden fee—it’s a breached identity. Financial institutions that fail to embed real-time identity protection are silently pushing customers into the arms of more secure competitors.

- 40M+ people impacted annually by identity theft

- Losses from synthetic fraud hit $2.7B in 2023

- 80% of customers expect built-in data protection—not optional upsells

💡 Takeaway: Don’t just sell security—embed it. Default protection builds loyalty that no cashback offer can replace.

Why Every Financial Product Needs Identity Protection—Now

The Threat Isn’t Just Real—It’s Evolving

- Synthetic identity fraud alone cost U.S. financial institutions $2.7 billion in 2023.

- 80% of consumers now expect financial brands to protect their personal data by default.

- Trust is now transactional: no protection, no loyalty.

Regulations Are Catching Up, Fast

New standards under GDPR, PIPEDA, and state-level laws like CCPA and Quebec Bill 64 mandate transparency and timely response to breaches. If you’re still relying on passive disclosures or weak alerts, you’re at risk.

What Is Embedded Identity Protection—and How Does It Work?

Think of it like built-in seatbelts for every product you offer. From checking accounts to auto loans to digital wallets—identity protection:

- Monitors SSNs, credit files, and dark web activity

- Sends real-time alerts for suspicious behavior

- Offers restoration services if fraud occurs

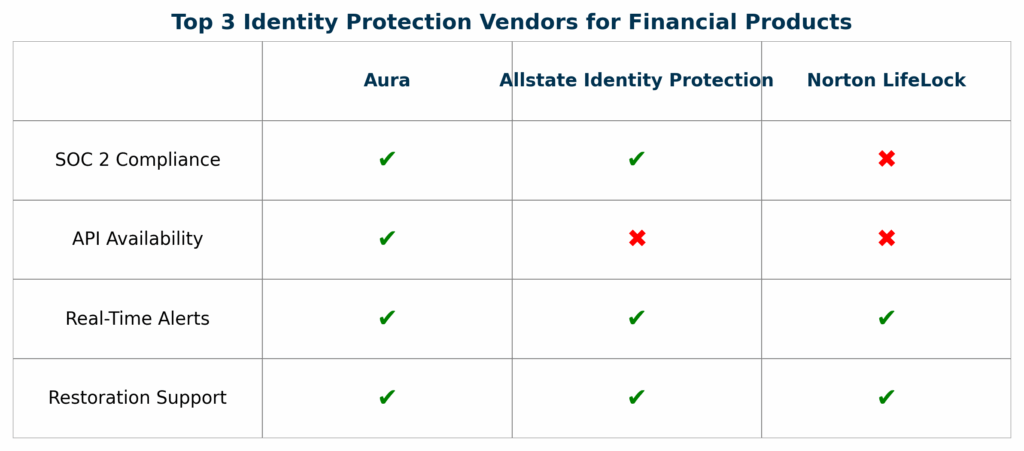

- Is often delivered via plug-and-play APIs from trusted vendors

How It Integrates Seamlessly

- Embedded in mobile apps and dashboards

- Presented at onboarding—no need for opt-in upsells

- Supported by APIs from providers like Aura, Allstate, and Norton

💡 Why Embedded Identity Protection Adds Value

- Attract More Customers: Security-first products differentiate fast.

- Boost Retention: Proactive alerts build daily trust and reduce churn.

- Drive Upgrades: Use identity coverage in tiered account structures.

🔍 Quote from Fintech CMO: “Adding identity alerts cut churn by 17% in one quarter.”

Why Identity Protection Adds Value Across the Customer Journey

Attract More Customers with Proactive Security

People shop for peace of mind. When your product markets itself as “identity-protected”, you gain an instant trust edge over competitors.

Boost Retention with Visible Safeguards

When users get proactive alerts from your app—not after the damage is done—you move from vendor to protector.

Drive Conversions with Tiered Value Offers

Use protection as a tiered benefit: “Basic” accounts without it, “Premium” accounts with it. Or offer it as an onboarding incentive.

💬 Visual suggestion: Quote pullout—Testimonial from a fintech CMO: “Adding identity alerts cut churn by 17% in one quarter.”

🛠️ How to Implement Identity Protection (Without Delays)

- Choose a SOC 2-Compliant Vendor – Make sure APIs are secure and scalable.

- Embed at Onboarding – Position it where users see it: apps, dashboards, welcome flows.

- Train Your Team – Support reps must act fast and communicate clearly during fraud alerts.

📋 Bonus: Add a “Privacy Promise” page and use trust badges sitewide.

How to Implement Identity Protection Without Derailing Your Roadmap

You don’t need to build it from scratch. But you do need to get it right.

Step 1: Choose a SOC 2-Compliant Vendor

Ensure they meet security standards and can scale with your offerings.

Step 2: Embed It in Product Flows

Make it visible on user dashboards, onboarding screens, and customer portals—not buried in terms and conditions.

Step 3: Train Support Teams to Respond Fast

A fraud alert is only helpful if your support team knows how to handle it confidently and empathetically.

Mistakes to Avoid (That Could Cost You Millions)

- Weak or vague user notifications: “Suspicious activity detected” won’t cut it—alerts must be specific and timely.

- Passive opt-ins: You must get clear, documented consent, especially in regulated markets like Quebec.

- Untrained reps: One mishandled fraud call can undo a year of trust-building.

⚠️ Mistakes That Could Cost You Millions

- ❌ Vague alerts like “Suspicious activity detected” – Customers need specifics

- ❌ Passive opt-ins – Especially risky in markets like Quebec under Bill 64

- ❌ Untrained fraud response – Mishandled alerts break trust instantly

Fix: Make fraud alerts clear, immediate, and backed by trained support.

The Competitive Edge of a Protected Customer Base

When a user feels protected, they stay longer, spend more, and tell others. This isn’t just security—it’s retention engineering.

And while your competitors are still trying to react to breaches, you’ll be the reason customers never worry in the first place.

Start Protecting Customers—Before They Leave for Someone Who Does

You don’t need to rip up your roadmap or hire a dozen engineers. You just need a partner who can embed identity protection with zero disruption.

Speak with an embedded protection specialist today

Get your personalized identity security plan—and see how fast you can go live.

📘 FAQ: Embedded Identity Protection

Q: How much fraud did synthetic identity theft cause in 2023?

A: $2.7 billion, primarily affecting unsecured financial services.

Q: What regulations require identity protection today?

A: PIPEDA (Canada), GDPR (EU), CCPA (U.S.), and Quebec Bill 64 all mandate proactive safeguards and breach transparency.

Q: What’s the difference between upsell protection and embedded?

A: Embedded protection is always on—users don’t need to opt in or pay extra to be covered.

Q: Is a third-party vendor required?

A: Not required, but preferred. Vendors like Aura, Norton, and Allstate offer plug-and-play APIs that are SOC 2-compliant and fast to deploy.